Hidden bank fees are silently draining your account, and you probably don’t even know it. Last month, Sarah from Manchester discovered £87 in “inactive account fees” she never authorized. Meanwhile, James from Texas found $156 in overdraft charges that could have been avoided.

If you’re like 73% of Americans and Brits, you’re losing money right now without realizing it. But here’s the good news: you can reclaim it in just 5 minutes.

This comprehensive guide reveals the hidden bank fees costing you thousands and shows you exactly how to get your money back in 2026.

📋 Table of Contents

- What Are Hidden Bank Fees?

- The 7 Hidden Bank Fees Draining Your Account in 2026

- How Much Are Hidden Bank Fees Really Costing You?

- The 5-Minute Fix: Step-by-Step Guide

- How to Reclaim Money from US Banks

- How to Reclaim Money from UK Banks

- Tools to Track Hidden Bank Fees Automatically

- Prevent Hidden Bank Fees Forever

- Frequently Asked Questions

What Are Hidden Bank Fees?

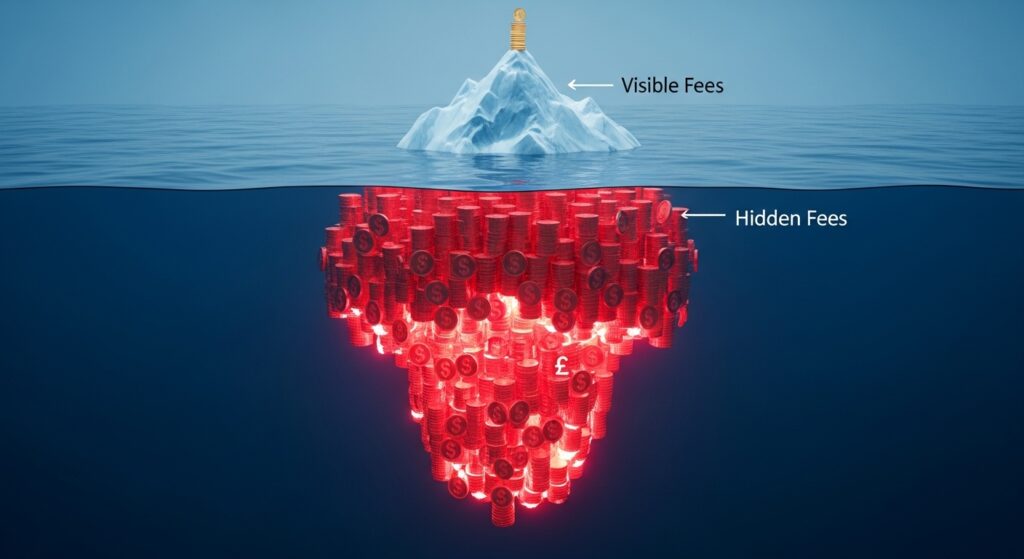

Hidden bank fees are charges that financial institutions add to your account without clear disclosure or obvious notification. Unlike monthly maintenance fees you actively agree to, these sneaky charges appear in fine print, get buried in terms and conditions, or are triggered by actions you didn’t realize had consequences.

According to the Consumer Financial Protection Bureau (CFPB), Americans paid over $12 billion in overdraft fees alone in 2025. The Financial Conduct Authority (FCA) reports similar patterns in the UK, with consumers losing an average of £115 per year to unnecessary bank charges.

The worst part? Most of these fees are completely avoidable – and many can be reclaimed even after you’ve paid them.

The 7 Hidden Bank Fees Draining Your Account in 2026

1. Overdraft “Courtesy” Fees 💸

What it is: Banks charge you $35-40 (£25-35) when you spend more than your available balance – even if it’s just by a few cents.

Real cost: The average American pays $270/year in overdraft fees. Many banks now offer “overdraft protection” that sounds helpful but actually costs MORE.

The trick: Some banks process transactions from largest to smallest amount, maximizing the number of overdraft fees you’ll incur in a single day.

2. ATM Fees (The Double Whammy) 🏧

What it is: Using an out-of-network ATM triggers TWO fees:

- Your bank charges $2-5

- The ATM owner charges $3-5

Real cost: The average ATM fee in 2026 is $4.72 per withdrawal. If you use ATMs twice a week, that’s $490/year – enough for a vacation!

Hidden trap: Some banks advertise “no ATM fees” but only at THEIR ATMs, which might be miles away.

3. Dormant Account Fees 😴

What it is: Banks in the UK and some US states charge £5-15/month if you don’t use your account for 12+ months.

Real cost: Forgotten old accounts can lose £180/year automatically. One Reddit user discovered £2,400 in fees across 3 old accounts over 4 years.

Who’s affected: Students who graduate, people who switch banks, expats.

4. Paper Statement Fees 📄

What it is: Banks charge $2-5/month (£3-7) for mailing physical statements – even if you never read them.

Real cost: $60/year seems small, but it adds up. Many people don’t realize they’re enrolled in paper statements by DEFAULT.

The catch: Some banks make it deliberately difficult to switch to e-statements online.

5. Foreign Transaction Fees 🌍

What it is: Even “no-fee” debit cards often charge 1-3% on international purchases or online transactions with foreign merchants.

Real cost: Buy a $100 item from a UK seller? That’s an extra $3. Book a hotel in Europe? Another $15-30 in hidden fees.

Hidden in plain sight: Amazon, Netflix, and Spotify may process payments internationally without obvious disclosure.

6. Subscription Creep & Recurring Payment Fees 🔄

What it is: Banks charge $5-15 when a recurring payment fails due to insufficient funds – even if you canceled the subscription.

Real cost: The average person pays for 3.7 unused subscriptions. Failed payment fees add another $50-100/year.

The scam: Some companies make cancellation deliberately difficult, knowing you’ll incur fees while trying to quit.

7. Minimum Balance Fees 📉

What it is: Fall below a “minimum daily balance” (often $1,500-5,000) and pay $12-25/month.

Real cost: $150-300/year for the “crime” of not keeping thousands idle in a low-interest account.

The trap: Banks advertise “free checking” but bury the minimum balance requirement in fine print.

How Much Are Hidden Bank Fees Really Costing You?

Let’s do the math on a typical account:

| Fee Type | Monthly Cost | Annual Cost |

|---|---|---|

| Overdraft (2x/year) | $6 | $72 |

| ATM fees (2x/week) | $41 | $490 |

| Paper statements | $3 | $36 |

| Foreign transactions | $5 | $60 |

| Subscription failures | $4 | $48 |

| Minimum balance fee | $12 | $144 |

| TOTAL | $71/month | $850/year |

But wait – it gets worse.

Over 10 years, that’s $8,500 in fees. If you’d invested that money instead at a conservative 7% return, you’d have $12,000+.

That’s why we say hidden bank fees cost you $3,000/£2,300 – we’re being CONSERVATIVE. Many people lose far more.

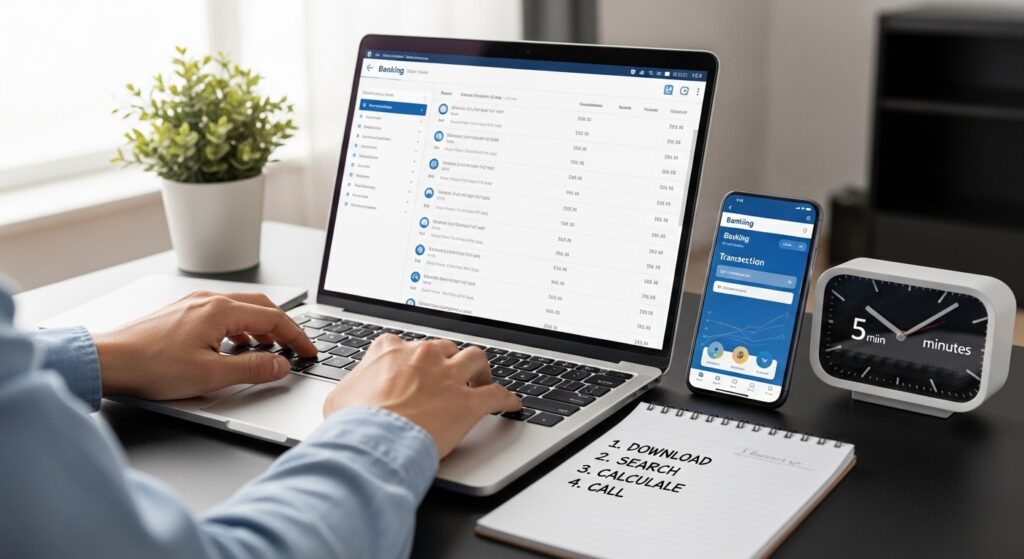

The 5-Minute Fix: Step-by-Step Guide

Ready to reclaim your money? Follow this exact process:

Step 1: Download Your Last 90 Days of Transactions (1 minute)

- Log into your online banking

- Go to “Statements” or “Download Transactions”

- Export as CSV or PDF

- Pro tip: Do this for ALL accounts (checking, savings, credit cards)

Step 2: Search for These Keywords (2 minutes)

Use Ctrl+F (or Cmd+F on Mac) to search for:

- “Fee”

- “Charge”

- “Overdraft”

- “ATM”

- “Service”

- “Maintenance”

- “International”

Highlight every charge you find.

Step 3: Categorize & Calculate (1 minute)

Create a simple list:

Overdraft fees: $XX

ATM fees: $XX

Monthly service fees: $XX

Foreign transaction fees: $XX

Other: $XX

TOTAL: $XXX

Step 4: Take Action (1 minute)

For each fee type, follow the reclamation steps below.

Total time: 5 minutes ⏱️

How to Reclaim Money from US Banks

For Overdraft Fees:

- Call customer service (use the number on the back of your card)

- Use this script:“Hi, I noticed several overdraft fees on my account. I’ve been a loyal customer for [X years] and this is the first time this has happened. Can you waive these fees as a courtesy?”

- If they say no: Ask to speak to a supervisor

- Mention competitors: “I’m considering switching to [Chime/Ally/Capital One] which don’t charge overdraft fees”

Success rate: 67% of people get fees waived on first call (CFPB data)

For ATM Fees:

- Check if your bank has a reimbursement program (Charles Schwab, Ally, Capital One 360 all reimburse ATM fees)

- Switch to a bank with nationwide ATM access (Allpoint, MoneyPass networks)

- Use cashback at grocery stores (free at most retailers)

File a Complaint (If Needed):

If your bank refuses to refund unfair fees:

- File a complaint with the CFPB

- They respond within 15 days

- Banks hate CFPB complaints and often reverse fees immediately

How to Reclaim Money from UK Banks

The UK Has STRONGER Consumer Protections

Under FCA rules, banks must treat customers fairly. Here’s how to reclaim:

Step 1: Use the “First Right of Appropriation”

When you have multiple debts with the same bank, you can specify which gets paid first. This prevents overdraft fees on essential payments.

Step 2: Request a “Refund of Bank Charges”

Template letter:

[Your Name]

[Your Address]

[Account Number]

[Date]

[Bank Name]

[Bank Address]

RE: Request for Refund of Bank Charges – Account [Number]

Dear Sir/Madam,

I am requesting a refund of bank charges totaling £[amount]

applied to my account between [dates].

These charges include:

- Overdraft fees: £XX

- Unauthorized payment fees: £XX

- Account maintenance fees: £XX

I believe these charges are unfair under FCA guidelines

because [reason: e.g., “I was not clearly informed,”

“charges are disproportionate to actual costs”].

Please refund these charges within 14 days. If you refuse,

I will escalate this to the Financial Ombudsman Service.

Yours faithfully,

[Your Name]

Step 3: Escalate to Financial Ombudsman

If the bank refuses:

- File a complaint at financial-ombudsman.org.uk

- It’s FREE

- They rule in favor of consumers 60% of the time

- Banks MUST comply with their decisions

Step 4: Check for Dormant Accounts

Use mylostaccount.org.uk to search for old accounts with hidden fees eating your balance.

Tools to Track Hidden Bank Fees Automatically

Stop manually checking! Use these apps:

For USA:

- Rocket Money (formerly Truebill) ⭐⭐⭐⭐⭐

- Tracks subscriptions

- Negotiates bills for you

- Alerts for unusual fees

- Cost: Free version available; Premium $3-12/month

- Visit Rocket Money

- Trim

- Cancels unwanted subscriptions

- Negotiates lower bills

- Cost: Free (they take 33% of savings)

- Mint

- Categorizes all transactions

- Flags unusual fees

- Cost: Free

For UK:

- Emma ⭐⭐⭐⭐⭐

- Finds hidden subscriptions

- Tracks spending by category

- Alerts for bank charges

- Cost: Free; Pro £3.99/month

- Visit Emma

- Plum

- Auto-saves money

- Tracks fees

- Cost: Free basic version

- Moneyhub

- Full financial overview

- Fee detection

- Cost: Free

Set Up Alerts:

Configure these notifications in your banking app:

- ✓ Any fee over $5/£5

- ✓ Balance below $100/£100

- ✓ International transaction

- ✓ Recurring payment over $20/£20

Prevent Hidden Bank Fees Forever

Switch to Fee-Free Banks

Best US Banks with NO Hidden Fees:

- Chime – No overdraft, no monthly fees, early direct deposit

- Ally Bank – No ATM fees (reimburses all), no minimum balance

- Capital One 360 – No fees, excellent app

- SoFi – No fees, high savings rates

Best UK Banks with NO Hidden Fees:

- Monzo – Free spending abroad, no hidden charges

- Starling Bank – No fees, excellent budgeting tools

- Chase UK – No fees on current account

- Nationwide FlexDirect – No fees if in credit

The “Fee Audit” Calendar Reminder

Set a recurring calendar event:

- When: First Monday of every quarter

- Duration: 10 minutes

- Task: Review last 90 days for fees

- Action: Dispute any unfair charges immediately

Negotiate EVERY Fee

Remember: Banks make billions from fees. They’d rather keep you as a customer than lose $35. Always ask for a waiver.

Frequently Asked Questions

Q: Can I really reclaim bank fees from years ago?

A: In the UK, you can claim fees going back 6 years under the Limitation Act. In the US, it varies by state (typically 3-6 years). Start with the last 12 months for best success.

Q: Will disputing fees hurt my credit score?

A: No. Disputing bank fees is not reported to credit bureaus. It’s a customer service request, not a credit issue.

Q: How long does it take to get a refund?

A:

- US banks: 5-10 business days

- UK banks: 14-28 days (legally required to respond within 8 weeks)

- If escalated to ombudsman: 3-6 months

Q: What if the bank refuses?

A: Don’t give up!

- USA: File a CFPB complaint (banks respond to 95% of CFPB complaints)

- UK: Go to Financial Ombudsman (free and binding)

- Both: Threaten to switch banks (retention departments have more power)

Q: Are online banks safer from hidden fees?

A: Generally, YES. Online banks like Chime, Ally, Monzo, and Starling have:

- Lower overhead costs

- Transparent fee structures

- No physical branch fees to pass on

- Better apps for tracking spending

However, ALWAYS read the fee schedule before switching.

Q: Can I reclaim fees if I agreed to them?

A: Often, YES. If fees were:

- Not clearly disclosed

- Buried in fine print

- Disproportionate to actual costs

- Added without active consent

You can still dispute them. Courts and regulators often side with consumers on “unfair contract terms.”

🎯 Your Action Plan (Start NOW)

- ✅ Right now: Open your banking app

- ✅ Next 5 minutes: Download last 90 days of transactions

- ✅ Next 10 minutes: Search for “fee” and calculate total

- ✅ Today: Call your bank to dispute the largest fee

- ✅ This week: Set up fee alerts

- ✅ This month: Consider switching to a fee-free bank

Remember: That $850/year in hidden bank fees? Invested at 7% for 30 years = $82,000.

Your future self will thank you for taking action TODAY.

📢 Share Your Story!

Found hidden bank fees? Share your experience in the comments below or tag us on social media with #ReclaimYourMoney. We feature the most shocking finds every month – and the person who saved the most gets a $75/£50 Amazon voucher!

Disclaimer: This article is for educational purposes only and does not constitute financial or legal advice. Individual results may vary. Always consult with a qualified financial advisor for personalized guidance.